Broken or Bent?

In his 1973 book, “A Random Walk Down Wall Street,” Burton Malkiel wrote that “a blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by the experts.” Investors who have followed seemingly sound diversification principles may now be wondering whether they should try their hand at dart-throwing, given the lackluster returns of recent experience.

Invest globally. Include some small caps. Tilt towards value stocks. All of these strategies have historically benefited investors from a risk and/or return standpoint over time, yet all have acted as a drag on performance over the last decade. And when things aren’t going your way in investing, years feel like decades and decades feel like centuries.

When what’s worked in the past no longer seems to be working, it’s no surprise that some folks opt to hit the reset button and start anew. These wholesale portfolio changes often come in one of two forms. Some simply invest in the rear-view mirror under the guise that they’re “keeping things simple.” Others get sucked into the zeitgeist of the moment, emboldened by the perception of easy money surrounding them, choosing to see if they have what it takes to be the next Warren Buffet Dave Portnoy. But before we all start day-trading with reckless abandon and dancing on the graves of supposedly “dead” asset classes and investing styles, I wanted to highlight a new piece from Research Affiliates.

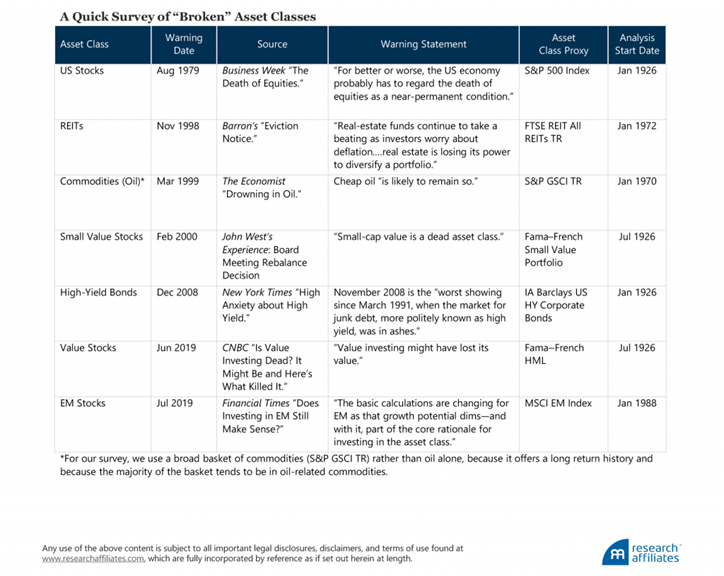

In this paper, they examine a non-exhaustive (and self-admittedly anecdotal) list of so-called “broken” assets from years past. In most cases, they found that the asset class in question was down, but not out – and certainly within the realm of historical ranges of expected returns. Here are the seven examples they analyzed:

Source: Research Affiliates

One interesting finding from their study was that in the three years leading up to the “warning date”:

…performance results relative to the S&P 500 tended to be more severe than absolute outcomes, suggesting that anchoring on mainstream assets is pervasive. For instance, three asset classes—REITs, small value stocks, and EM stocks—managed to deliver returns slightly above their long-term median levels in the three years preceding the declarations’ warning that they were defunct. But when viewed relative to mainstream assets, all three suffered relative shortfalls, trailing US stocks by up to 14% a year over the three-year period preceding their respective warning dates.

They also highlight the missed opportunities by those who succumbed to the temptation to bail. The researchers looked at the five-year returns of assets declared broken OR that fell into the bottom decile of their historical returns. What they found is that in most cases, these left-for-dead assets came roaring back. Specifically:

- 88% of the observations delivered a positive return in the subsequent five years.

- The average five-year return was approximately 80%.

- The cumulative excess return of REITS, commodities, small value stocks, and high-yield bonds relative the S&P 500 averaged 101%, or 15% a year.

![]() Source: Research Affiliates

Source: Research Affiliates

The easy thing to do when confronted with disappointing results is to assume something is broken. But the reality is that all worthwhile long-term strategies share one thing in common; they all inevitably bend to varying degrees of pain. Very few, however, ultimately break.

Allow me to share three date periods with you:

- 1929-1943 (15 years)

- 1966-1982 (17 Years)

- 2000-2012 (12 Years)

What do each of these distinct time periods have in common? They are all decade-plus spans in which the S&P 500 – everybody’s favorite reference point, anchor and all-around index darling – underperformed T-Bills! Those are incredibly long times to lag the risk-free rate, testing the patience of even the most stoic investors.

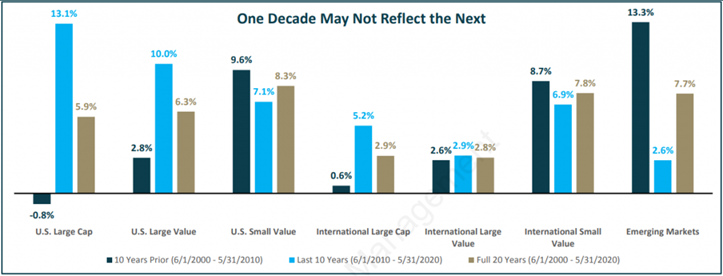

It would have been a grave mistake to exit U.S. Large Cap stocks following those rough stretches for the S&P 500. It would be similarly unwise to cast aside today’s misfit toys, particularity those that are attractively priced for the decade ahead. In life and in markets, the next decade seldom looks like the last.

With that in mind, I’ll just leave this here:

Source: Savant Capital Management

Indices are unmanaged, do not reflect fees and expenses and are not available as direct investments. Returns are calculated in U.S. dollars and reflect the reinvestment of dividends and other earnings.

Additional Reading:

A Quick Survey of “Broken” Asset Classes (Research Affiliates)

About the author

Phil Huber, CFA, CFP®

Phil is the Head of Portfolio Solutions for Cliffwater, a leading alternative investment adviser and fund manager. Prior to joining Cliffwater in 2024, Phil was the Chief Investment Officer for Savant Wealth Management, a multi-billion dollar wealth management firm. Phil has been involved in the financial services industry since 2007. He earned a bachelor’s degree in finance from the Kelley School of Business at Indiana University. He is a member of the CFA Society of Chicago. More about me here. Twitter: @bpsandpieces

Get on the List!

Sign up to receive the latest insights from Phil Huber directly to your inbox.