Family, Food, Football and Factors

“This year I am thankful for the worst performing assets in my portfolio” – said no one ever during Thanksgiving dinner

The other night, as I sat at home polishing off what remained of last week’s leftovers, I couldn’t resist the temptation to write a blog post (albeit a late one) connecting Thanksgiving to investing. Like many Americans, my holiday was filled with loved ones, plenty of pigskin, and lots of turkey and mashed potatoes – all things that we should be grateful for! As investors, something we should also be thankful for is the often underappreciated power that diversification can have on a portfolio.

The unfortunate reality is that most people would rather send diversification to the kids’ table instead of giving it thanks. This is largely because investors often miss the forest for the trees by focusing on individual components rather than the portfolio as a whole. My pal Brian Portnoy elaborates:

Being truly diversified means that there almost always will be a part of your portfolio that is sucking wind. (Big note: if every piece of your portfolio is working really well, it means one of two things: you’re incredibly lucky or you are not actually diversified. I would assume the latter.)

But what’s the big deal about that? Indeed, owning underperformers is built into the definition. While statistically true, there is an unspoken behavioral component to this experience: We hate owning losers. And we fixate on the negative, drumming up feelings of regret and “if only” I (or my adviser) had tilted more toward fill-in-the-blank.

In other words – to borrow a phrase from Brian – diversification means always having to say you’re sorry.

So how do we correct this behavior to help ourselves focus on the bigger picture? The first step is figuring out what true diversification really is. People often cite the Great Financial Crisis of 2008-09 as evidence of diversification failing as correlations spiked and almost all risk assets suffered significant drawdowns. But it wasn’t diversification that failed in this environment, it was the understanding and implementation of it that did.

A silver lining of the GFC were some of the lessons in portfolio construction we learned as a result of some of the faulty assumptions we made. For example:

- Filling out the Morningstar style box isn’t enough: manager diversification within small-cap growth means nothing when the world is on fire.

- D.I.N.O. won’t insulate you from market shocks: satellite asset classes such as Emerging Markets, REITs, Commodities, and Junk Bonds were all the rage in the mid/late 2000s (and still are today) but when push came to shove in 08-09 they offered Diversification In Name Only. I’m not knocking any of these categories as investment choices (I own several of them), but a misalignment between expectations and reality can only lead to poor results. Risk assets are called that for a reason, don’t get it twisted.

- Not all bonds are alike: just because something has the word “bond” or “income” in the name does NOT guarantee it is safe or defensive. Not by a long shot. A pre-crisis 60/40 portfolio in which the “40” was made of of credit-sensitive income investments may have felt great when things were calm, but man did it magnify the pain when s*@# hit the fan. Time and time again, we are reminded: yield giveth and yield taketh away.

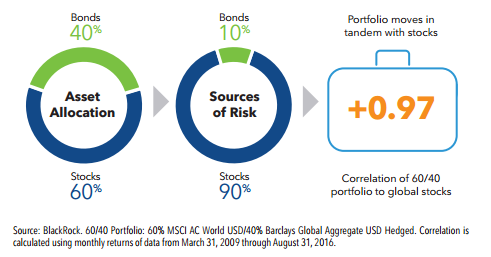

- Dollar allocation is not the same as risk allocation: Take this illustration from BlackRock of a hypothetical 60/40 portfolio. Although 40 percent of the portfolio is in bonds, the risk of the portfolio is dominated by stocks due to the volatility of equities dwarfing that of fixed income. The result is a portfolio that is nearly perfectly correlated with equities.

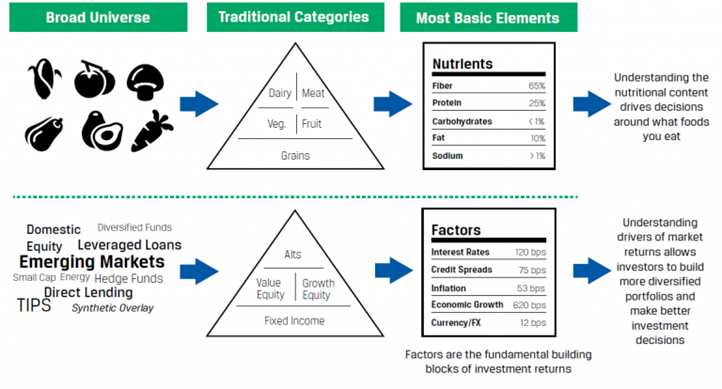

From the ashes of all these hard-earned lessons emerged a new framework that provided us with a fresh way of thinking about diversification: factor investing. Factors can be thought of as the underlying drivers of return that exist due to compensation for rewarded risk, persistent behavioral biases exhibited by investors, or structural market inefficiencies. These factors can be divided into two broad categories: Macroeconomic Factors (across asset classes) and Style Factors (within asset class). Kudos to BlackRock for the below illustration that highlights and summarizes some of the more common and widely accepted factors.

Source: BlackRock

Industry legend Larry Swedroe had the following to say in an interview with ETF.com on the benefits of combining different factors together:

You want to add factors that not only have premiums and meet the tests I laid out, you want to add a factor portfolio that also has low-to-negative correlation to the other assets in your portfolio, because that’ll add a diversification benefit.

The second thing is research shows that diversification across factors that have premiums and low correlations have historically resulted in significantly more efficient portfolios. Low correlation dampens the volatility of the overall portfolio.

For most people, applying a factor-based approach to investing may not be that intuitive thing in the world so I thought that it might be helpful to frame it a few different ways. And wouldn’t you know it, they all start with the letter F. Funny how it works out like that, right?

Family

Ben Hunt of Salient Partners writes a regular newsletter called Epsilon Theory. Highly recommended if you aren’t already a reader. In one of his recent pieces, he touches on the concept of everyone and everything having a “job to do” and uses the Hunt family dogs as an example (emphasis mine):

The Hunt family has three dogs, each with a distinct job. The German Shephard’s job is to protect. The Sheltie’s job is to herd. The Golden’s job is to love. Each dog is very good at its job, sometimes in an annoying way (particularly the Sheltie), but they’re oh-so happy with what they do well, and it fits our entire family dynamic. There are sacrifices we make for having this particular pack, like we can’t have any other dogs drop in for a visit or else the German Shephard might eat them, but the positives far outweigh the negatives. We’re a solid pack, and there’s nothing quite like that feeling of knowing that the dogs are there for you and you for them, and that the entire Hunt family — human and dog alike — is stronger not just in fact but in spirit for giving ourselves over to the pack.

It’s the same with investment portfolios. Every dog needs a job, and every investment does, too. No single dog can be all things to all people, and neither can a single investment. Nor can any pack of dogs accomplish anything and everything you like. The biggest mistake people make when they get a dog is trying to make the dog fit into the life they wish they led, rather than the life they actually lead. You better know thyself before you get a dog, much less a couple of dogs, and it’s exactly the same thing with making an investment…

…they’re mistaking a quality of the portfolio — diversification — for a job of an individual investment. Asking an investment to provide diversification is like asking a dog to provide pack stability. It’s just not within their power to do this. Portfolio diversification and pack stability emerge from the proper organization and job assignment of the individual members of the portfolio or pack, not the other way around. If someone tells you that their alternative strategy is “a diversifier”, your question should be “Relative to what?” if you’re in a generous mood, something a little more snippy if you’re not. The question you need answered is what job does the strategy perform in your portfolio. How should I expect it to behave under what conditions? Then you can decide for yourself how that job fits with the other jobs your other investments are doing.

Families are a unit and portfolios are too. We all get frustrated with family members from time to time, but it doesn’t mean we don’t love them. Each person (usually) brings something unique to the table that helps support overall pack stability. It’s okay to get upset with individual investments too – after all, no one likes losing money – but try not to let a little squabble among portfolio siblings turn into full-blown family warfare!

Food

Another helpful way to view things through a factor-based lens is by comparing investments to food. BlackRock’s Andrew Ang covers this analogy in great detail in his epic book Asset Management: A Systematic Approach to Factor Investing:

Factors are to assets what nutrients are to food…Investing right requires looking through asset class labels to understand the factor content, just as eating right requires looking through food labels to understand the nutrient content…

Source: BlackRock

Most of us filled our Thanksgiving plates with a smorgasbord of different foods covering an array of unique colors – brown gravy, green beans, orange carrots, red cranberry sauce. In fact, it probably resembled a somewhat messier version of the pie charts we all see on our account performance reports. But while the main course and side dishes were diverse in taste and texture, the underlying nutritional content was probably not as robust. Adding additional line-items to your statements by buying new funds may feel diversifying, but if all you’re doing is increasing the levels of already widely-held factors, then you aren’t going to have a well-balanced diet portfolio.

Football

Football is a game of three phases: offense, defense and special teams. Translating offense and defense to portfolio roles is rather easy:

Stocks = Offense

Bonds = Defense

But what about special teams?

Many investors and advisors struggle when it comes to compartmentalizing non-traditional and alternative investments. They have difficulty determining where to source the allocations from and how to set proper expectations for risk, return and role in a portfolio. If you think about it, framing alternatives as the special teams of a portfolio makes a lot of sense.

I’ll preface this argument with a couple of things. First, alternatives are not a prerequisite for a successful investment experience. In fact, an argument can be made that the majority of investors are better off keeping things simple as deviating into the unfamiliar may lead to poor behavior. Second, most of what passes for “alternative” these days are either:

a) too expensive relative to comparable options or value added

b) Not hedged/uncorrelated enough to the rest of the portfolio

c) Ran by asset managers with no prior experience in such strategies that are suffering from the F.O.M.O. on the current zeitgeist.

d) All of the above

Now that that’s out of the way, back to alternatives as special teams. If you’re an NFL team and you’re hanging your Super Bowl hopes on what your special teams can do while completely ignoring the offensive and defensive phases of the game, you’ll find yourself on the fast track for the #1 pick in the next year’s draft. Seasons aren’t won and lost on field goals, blocked punts and kick returns. But many individual games often come down to these very circumstances. In fact, two Sundays ago a new record was set for the number of missed extra points in a single week, a few of which directly impacted the final result of the game. The point is that while special teams is not the most exciting or important aspect of football, it can still be extremely valuable. Similarly, a portfolio with alternatives as the sole focus is probably not the best idea. But augmenting a traditional stock/bond mix with a well-rounded suite of uncorrelated assets and strategies with economically intuitive and differentiated return drivers can help a portfolio cross the goal line.

An effectively and efficiently diversified portfolio is the result of the whole being greater than the sum of its parts. By focusing less on the parts and more on the whole, we all might find something we are truly thankful for.

Additional Reading:

Diversification Means Always Having To Say You’re Sorry (The Investor’s Paradox)

New Swedroe Book: ‘Your Complete Guide To Factor Investing’ (ETF.com)

You Had One Job (Epsilon Theory)

Asset Management: A Systematic Approach to Factor Investing (Amazon)

About the author

Phil Huber, CFA, CFP®

Phil is the Head of Portfolio Solutions for Cliffwater, a leading alternative investment adviser and fund manager. Prior to joining Cliffwater in 2024, Phil was the Chief Investment Officer for Savant Wealth Management, a multi-billion dollar wealth management firm. Phil has been involved in the financial services industry since 2007. He earned a bachelor’s degree in finance from the Kelley School of Business at Indiana University. He is a member of the CFA Society of Chicago. More about me here. Twitter: @bpsandpieces

Get on the List!

Sign up to receive the latest insights from Phil Huber directly to your inbox.