Multifactor Multiplicity

Last week, Bloomberg’s Tom Psarofagis (Sarah-Fay-Guess) tweeted out this list of multifactor U.S. equity ETFs that showed their 2018 performance relative to the S&P 500, as proxied by SPY:

Only two of the funds outpaced SPY, and a number of them underperformed dramatically. Here is a visual look at the performance of these ETFs in 2018 (I omitted the Invesco fund as it is slated for liquidation):

What is not surprising, given that SPY finished the year in the red, is that all of the other ETFs ended the year in negative territory as well. What is a bit surprising, perhaps, is just how wide the spectrum of performance was between the best and worst. After all, how different can these multifactor funds be from one another?

As it turns out, a lot.

At the surface level, it might seem reasonable to assume that the disparities between these funds are negligible. This couldn’t be further from the truth. The devil (or in this case the HmL devil) is always in the details and as my friend Corey Hoffstein likes to point out, the What, How and When matter a great deal when it comes to evaluating and selecting multifactor funds.

Source: Newfound Research

A number of critical questions must be addressed by advisors and other professional investors during the due diligence process, such as:

- What factors are being targeted?

- How are those factors being measured?

- Are mid-cap and small-cap stocks included?

- What are the underlying fund expenses?

- Is it an ETF or a mutual fund?

- Does the factor exposure change over time or is it relatively static?

- Are there any sector constraints relative to a benchmark or parent index?

- How diversified or concentrated is the portfolio by number of holdings?

- What is the tracking error of the fund? In other words, how different am I going to look versus the benchmark in a given period?

- How often and when does the fund rebalance its holdings?

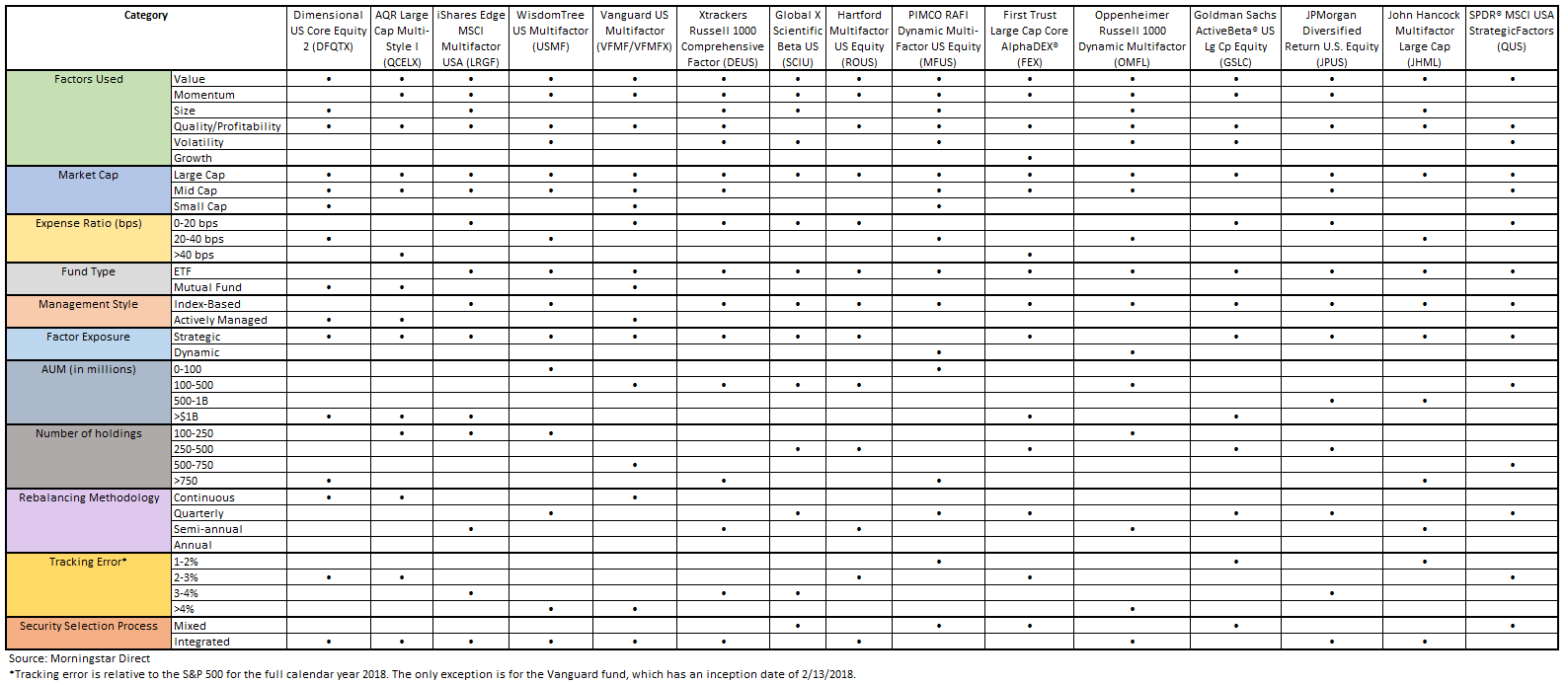

I attempted to compile answers to those questions (and others) in this chart that compares all of the funds from above, plus a handful of others from DFA, AQR, Vanguard and State Street. (Click to enlarge.)

There is a lot going on in the image above that might be difficult to discern, but the one thing I hope you take away is that there is a lot of nuance here.

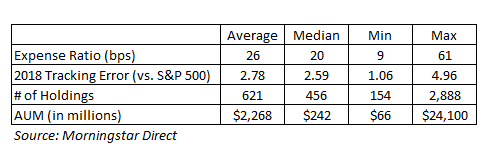

I also summarized some of the more numerical categories:

There were some really interesting findings from this research. For example:

- While each fund has its own unique factor mix, all fifteen included some allocation to the value factor. No other factor was included in every fund.

- The most concentrated fund by holdings was LRGF from iShares, with 154 securities. On the other end of the spectrum, DFQTX from Dimensional has nearly 3,000 holdings.

- The Dimensional fund is also by far the largest fund, with over $24 Billion in AUM. Only four other funds have over $1 Billion. Meanwhile, several funds are under, or just barely over, $100 Million.

- Vanguard’s Multifactor Fund is the only fund available in both mutual fund and ETF share classes.

- Low cost is the name of the game with multifactor funds, with a median expense ratio of 20 bps. GSLC from Goldman Sachs the cheapest, with rock-bottom fees of 9 bps. FEX from First Trust is the priciest, coming in at 61 bps.

- While GSLC is the cheapest, it’s also the most timid when it comes to deviating from the benchmark. It had the lowest tracking error to the S&P 500 at 1.06. The three funds with the highest tracking error came from Vanguard, WisdomTree, and Oppenheimer.

- Twelve out of the fifteen funds are index-based, whereas three are actively managed: Dimensional, AQR, and Vanguard.

Now unfortunately, nothing above contains any insight or clairvoyance as to which funds will perform best over time. So why even bother with the exercise? To illustrate the importance of looking under the hood of funds that on the surface seem similar, but at a granular level are much less homogeneous than meets the eye.

As multifactor funds continue to grow in popularity, knowing what you own and why you own it is key to sticking with a strategy through the inevitable ups and downs.

About the author

Phil Huber, CFA, CFP®

Phil is the Head of Portfolio Solutions for Cliffwater, a leading alternative investment adviser and fund manager. Prior to joining Cliffwater in 2024, Phil was the Chief Investment Officer for Savant Wealth Management, a multi-billion dollar wealth management firm. Phil has been involved in the financial services industry since 2007. He earned a bachelor’s degree in finance from the Kelley School of Business at Indiana University. He is a member of the CFA Society of Chicago. More about me here. Twitter: @bpsandpieces

Get on the List!

Sign up to receive the latest insights from Phil Huber directly to your inbox.