The Paper Trail: A New Paradigm

Welcome to the February edition of The Paper Trail!

We'll kick off this month's installment with my latest white paper for Cliffwater, which tackles the pros and cons of payment-in-kind ("PIK") income in direct lending.

PIK income has become a lightning rod of debate in private debt. While it can offer borrowers flexibility and potentially enhance lender returns, it may also introduce additional credit risk and uncertainty in cash flow realization.

As private debt markets evolve, understanding when PIK is a feature of financial strength versus a sign of distress is crucial for investors navigating the asset class. My paper explores the mechanics of PIK income, its historical trends, and the trade-offs that investors must consider.

As private debt markets evolve, understanding when PIK is a feature of financial strength versus a sign of distress is crucial for investors navigating the asset class. My paper explores the mechanics of PIK income, its historical trends, and the trade-offs that investors must consider.

Why it matters: Not all PIK income is created equal. While it can be a valuable tool in the right circumstances, indiscriminate use can signal deteriorating credit quality and heightened risk.

Additional topics covered in this month's research roundup include:

- Equity long/short tailwinds

- Growth equity in private markets

- High-grade corporate debt vs. Treasury bonds

- International quality stocks

- Royalties as an asset class

- The resiliency of systematic investment strategies

- Private equity's outlook for 2025 and beyond

- Balancing probabilities and payoffs

- Portable alpha frameworks

- A record year for secondaries

- Emerging market return drivers

“bps” (reading time < 10 minutes)

Is payment-in-kind (PIK) income a feature or a bug of direct lending?

"PIK income, which allows borrowers to capitalize all (or a portion) of their interest expense rather than pay in cash, has become a lightning rod of debate in the asset class. To some, it represents a creative financing solution that aligns with the needs of borrowers in growth phases. To others, it raises red flags about credit risk and the true quality of the borrower."

PIK and Choose: The Pros and Cons of Deferred Income in Direct Lending (Cliffwater)

Are the headwinds that have faced equity long/short (ELS) strategies stating to dissipate?

"Fundamental ELS strategies have faced challenges since the GFC, but the tide may be turning. The recent increase in cash yields and higher equity dispersion create a more favorable environment for the short book and will offer opportunities for managers to distinguish themselves."

A More Appealing Environment for Equity Long/Short Strategies (Cambridge Associates)

Can growth equity strategies in private markets continue to deliver venture-like upside with buyout-like risk?

"Large-cap private equity firms continue to acquire businesses backed by small and midsize growth equity managers, underscoring the resilience of exit opportunities in the growth equity space and sustained demand in the lower middle market."

Revisiting the Growth Equity Market Opportunity (StepStone)

Is Microsoft a safer credit than the U.S. government?

"While the U.S. government might seem like a safe bet due to its ability to print money and collect taxes, the financial metrics and credit ratings tell a different story. In a world where many people's "ultimately safe bet," Treasuries, aren't as rock solid as they once seemed, it might well be time to give high-grade corporates issuers a second look."

Would You Rather Lend to the US Government or Microsoft? (DoubleLine)

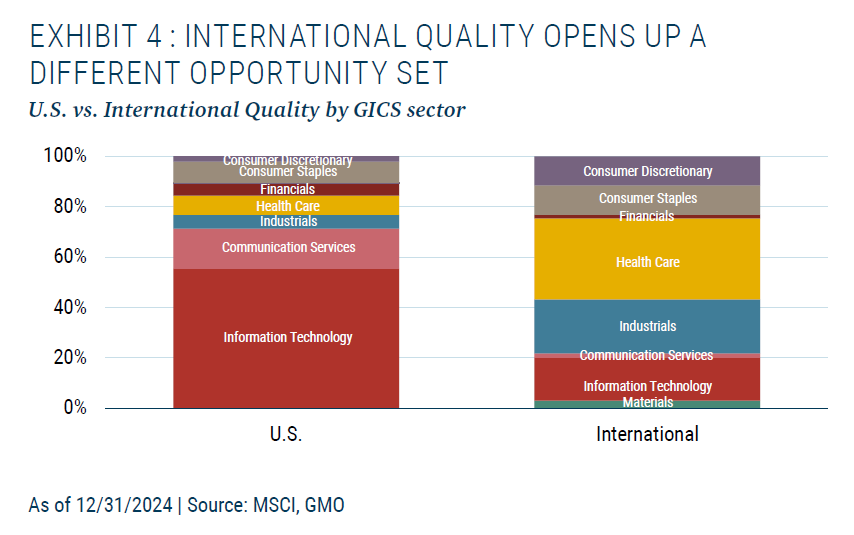

Are international quality stocks a potential antidote to U.S. large cap growth risk?

"The International Quality universe is much more diversified than the equivalent U.S. Quality universe, which currently has 71% in broad Technology. Moreover, as noted above, International Quality businesses are often the leaders in industries where the U.S. is underrepresented.

International Quality: The Perfect Pairing for Your U.S. Large Cap Portfolio? (GMO)

Are royalties a unique asset class?

"The structured nature of many royalty investments provides clarity and control over payment terms and durations, akin to private credit instruments. However, unlike private credit, royalties also offer potential upside driven by the underlying asset’s performance. This places the risk-return profile of royalty investments between that of private credit and private equity."

Royalties: A Primer (Partners Group)

“pieces” (reading time > 10 minutes)

Are systematic investment approaches more resilient to market concentration than discretionary stock pickers?

"The theory underlying our hypothesis hinges on the way discretionary and systematic managers take risks. Discretionary managers hold concentrated portfolios with far fewer securities than typical systematic managers. Some likely had no exposure at all to some of the Mag-7 companies, while others held large positions in them. This concentrated approach exposes them to binary have/have-not outcomes when a few stocks are driving market performance. Systematic managers are not exposed to this risk in the same way because they generally spread their active risk across many small bets, and often explicitly control any sector and industry risks. A typical systematic manager would hold all of the Mag-7 stocks, with some of them slightly overweight and some slightly underweight, and similarly would be only slightly over- or underweight any given sector or industry."

A New Paradigm in Active Equity (AQR)

What is the outlook for private equity in 2025 and beyond?

"For private equity operators, there has never been a greater need to focus on value creation to drive returns, given increasing purchase prices (as a multiple of EBITDA) and lengthening holding periods. While multiple expansion has driven private equity returns for a decade, steeper entry multiples and the heightened cost of leverage mean this lever is unlikely to persist for the next decade."

Global Private Markets Report 2025: Private equity emerging from the fog (McKinsey)

Do investors overvalue probabilities relative to expected payoffs?

"The Babe Ruth effect highlights that it is not only how often you are right that matters (probability) but how much you make when you are right versus how much you lose when you are wrong (payoffs)."

Probabilities and Payoffs: The Practicalities and Psychology of Expected Value (Counterpoint Global)

Can a portable alpha framework solve the Magnificent Seven's diversification problem?

"By separating alpha from beta, we can diversify the alpha source. Specifically, in the case of the Magnificent Seven, portable alpha facilitates alpha sources from outside of equities, thereby enabling us to move away from stock picking. In this regard, we examine alpha in the form of an allocation to multi-strategy and trend following strategies."

Portable Alpha: Solving the Magnificent Problem (Man Group)

Will the momentum from 2024's record year for secondaries volume continue in 2025?

"Global secondary volume of $162 billion in 2024 surpassed our beginning of year estimate of ~$130 billion as the industry posted volume records across both the LP and GP-led markets. We expect that growth will continue in 2025, propelled by strong supply of both LP portfolios and GP-led transactions matched with significant demand and a well-capitalized buyside."

Global Secondary Market Review (Jefferies)

Which return drivers have been responsible for EM underperformance since the GFC?

"Emerging markets as a whole experienced declining margins, which affected earnings growth. Within EM ex China, muted earnings growth and currency depreciation against the USD negatively impacted returns. Valuation expansion, particularly in India, was a key source of returns, but not so in China, where valuation-multiple expansion was modest."

Long-Term Investing in Emerging Markets (MSCI)

About the author

Phil Huber, CFA, CFP®

Phil is the Head of Portfolio Solutions for Cliffwater, a leading alternative investment adviser and fund manager. Prior to joining Cliffwater in 2024, Phil was the Chief Investment Officer for Savant Wealth Management, a multi-billion dollar wealth management firm. Phil has been involved in the financial services industry since 2007. He earned a bachelor’s degree in finance from the Kelley School of Business at Indiana University. He is a member of the CFA Society of Chicago. More about me here. Twitter: @bpsandpieces

Get on the List!

Sign up to receive the latest insights from Phil Huber directly to your inbox.